I have the great pleasure in introducing you to a new writer, Jared Sleeper, who will make regular contributions to this blog. We were very excited to have Jared to join Matrix Partners recently as he is a truly exceptional individual. Jared grew up in Maine working in his family’s grocery store. He had a deep passion for business and investing from a young age. At Harvard, he led the college’s largest investing club, growing the membership significantly and refocusing it on fundamental research and thesis-driven investing. As part of this work, he represented Harvard at the 2013 Cornell Undergraduate Stock Pitch Challenge where his team took the top prize.

Putnam Investments, a sponsor of the competition, hired him as an investor immediately thereafter. After less than two years he was promoted (becoming the youngest analyst at the firm) and was responsible for all small and mid-size public tech company investments. He invested in spaces ranging from cybersecurity to consumer internet to marketplaces, but he had a special affinity for and focus on SaaS. On his recommendations, Putnam successfully invested hundreds of millions of dollars in SaaS companies including Netsuite, Wix, Shopify, ServiceNow, Everbridge and Instructure. Jared sees the world through the eyes of a public company investor in some of the most successful SaaS companies, which brings a different perspective to our readers. But he is also just simply one of the smartest (and nicest) people I have had the pleasure of meeting, and I think you will enjoy his writing. He posts shorter form content on tech investing at his personal blog Sleeperthoughts.com.

As one of the early bloggers to write about LTV:CAC, and having introduced the goal that this should be greater than 3 for a healthy SaaS business, I later realized that I had made a significant mistake in not telling my readers when it would make sense to compute LTV and CAC. Many readers were trying to compute LTV:CAC before they had any semblance of a repeatable, scalable sales process, and you could see that their CAC numbers would likely change as they worked to scale their sales and marketing approaches.

In this post, Jared explains common mistakes we see founders make in calculating LTV:CAC and when and how to calculate the metric to make it most effective.

–David Skok, Author of forEntrepreneurs

Intro

At Matrix, we are big fans of SaaS metrics. We love to help our portfolio companies understand the key levers they can pull to solve bottlenecks in their sales funnel, reduce churn, and increase expansion revenue from up/cross-selling. While we’re delighted to see that more and more startups are embracing metrics-driven approaches to making go-to-market decisions and pitching to potential investors, we’re aware that we’ve helped unleash a bit of a monster on the startup scene in the form of the LTV:CAC ratio. We often see founders making four key mistakes on LTV:CAC:

1) Calculating the metric too soon.

2) Hyperfocusing on the specifics of how it is calculated.

3) Not using LTV:CAC to drive business decisions.

4) Not fully understanding how it influences decisions investors make.

David and I have discussed these challenges at length, and in the rest of this post we’ve teamed up to tackle some of the key issues: when should a company calculate this metric with its own data in the first place, and what are some of the right ways to use it as an early stage startup?

Why we calculate LTV:CAC in the first place

LTV:CAC is a tool for measuring the efficiency of a crucial part of the business, the sales and marketing funnel. It does this by asking a simple question: is a customer worth more (LTV – Lifetime Value) than what it costs to sell to them (CAC – Cost to Acquire a Customer)? For founders and investors alike, the framework can help provide answers to important questions like:

- Even though, like most SaaS companies, this company is losing money, will it ever become profitable?

- Is the go-to-market efficient, overall and at the margins?

- Where/when to invest more in sales and marketing?

- How much to invest in sales and marketing?

- Which customer types, products, business lines, etc. are the most profitable?

Note that all of these questions are fundamentally about marginal LTV:CAC. (Note: David informed me that I let my economics background slip in here. If “marginal” is a foreign concept, here’s a great explainer). Rephrasing more simply, to make decisions about what to do in the future it is important to know how much LTV will result from the next unit of CAC, whether that means spending another $1,000 on Google adwords or hiring a new sales rep. So LTV:CAC is used for making predictions about future outcomes, based on past results, that will help drive important business decisions.

When should a startup start calculating LTV:CAC?

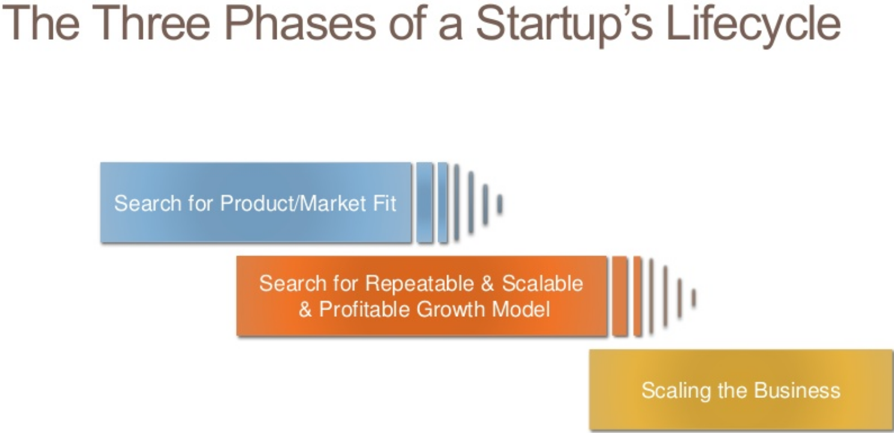

In order to use LTV:CAC to guide decision making, the data flowing into the calculation needs to be meaningful enough to have predictive value. For example if a founder is closing deals herself, those deals (and her salary) probably don’t belong in the LTV:CAC calculation, as we learn very little about how productive a newly hired sales rep would be. Similarly, for startups acquiring customers through pre-existing relationships, or promising margin-crushing customer success attention to the first dozen customers, those deals probably don’t give good insights into what a more normalized go-to-market will look like. David’s concept of the “three stages of a start-up” captures this well:

David Skok (DS): I think of a startup as having three stages: the search for product/market fit, the search for a repeatable, scalable and profitable growth process, and the expansion phase. What I should have emphasized when talking about LTV:CAC is that the numbers will only really be meaningful and reliable when you have found a repeatable and scalable growth process. So if all your early leads are coming from inbound lead flow, or paid search, don’t assume that those channels will scale infinitely. A more typical experience is that as a company needs to scale lead flow, it is forced to add more expensive channels, sometimes including expensive lead generation through SDRs (Sales Development Reps).

In short, LTV:CAC calculated from company data becomes relevant when the growth process becomes both repeatable and scalable, and the data feeding into it is instructive as to what future outcomes will be.

How start-ups can practically use LTV:CAC when the time is right

When the scalable go-to-market process is underway, LTV:CAC quickly becomes indispensable for making business decisions. Here are some concrete examples of questions they are well suited to answering:

1) Which size or type of customer is most efficient to acquire? Perhaps enterprise customers have higher CAC but much lower churn and thus higher LTV. Obviously, the customer set with the higher LTV:CAC, all else equal, deserves more incremental investment. But it is also helpful to look at the less profitable customers and ask the question of whether there is something that can be done to make them more profitable.

DS: At HubSpot there were two customer types (personae) in the early days: Owner Ollie and Marketing Mary. Owner Ollie was the owner of a very small business and did their own marketing. Marketing Mary worked for a slightly bigger company and was in charge of marketing. For awhile the company had a hard time choosing which persona to initially focus on. This was holding back success, as the optimal product needed for each persona was different. Finally, the company used LTV:CAC and Months to Recover CAC as metrics to evaluate each persona, and quickly discovered that Marketing Mary was a more profitable customer. That solved the discussion, and the focus shifted to Mary.

Later on the company discovered that selling to Owner Ollie through a channel partner produced even better LTV:CAC than selling to Marketing Mary. This was because the channel were doing the hard work of helping Ollie write the content, and use the software. But without the LTV:CAC metric, we wouldn’t have known this.

2) How much can feasibly be spent to acquire a given type of customer? This is related but in lower-touch applications like high-velocity SaaS and B2C it is critical for tuning marketing spend. Many online retailers need to calculate how much they are willing to pay for a referral- LTV:CAC provides the answer, as if the LTV of a new customer is $100 and the target LTV:CAC ratio is 3:1, a good referral is worth ~$30.

DS: There is an important caveat here. While in theory a well calculated LTV:CAC ratio provides this answer, startups must also watch a related metric, “months to recover CAC.” If it takes too long to recover marketing spend, a startup may require unworkable amounts of capital. For this reason, I consider months to recover CAC an even more powerful metric in the early stages of a startup’s life. See my post here for more details on months to recover CAC and other SaaS metrics.

3) How many sales reps should be hired? Depending on what a startup decides the appropriate LTV:CAC target is (again, based on management’s understanding of the assumptions involved), it should bring on as many units of growth (sales reps) as it can so long as the marginal unit economics hold up and the rest of the business can manage it. If the unit economics are working, underinvesting in S&M is not “prudently conserving cash,” it is leaving money on the table, and creating an opportunity for competitors to grow faster and win the market.

Where LTV:CAC can be useful before you have found a repeatable sales process

While we are saying that your LTV:CAC numbers will not be accurate until you have found a repeatable and scalable sales process, we are not suggesting that you should not be thinking about these metrics ahead of that time. There is still significant value for founders in thinking about LTV:CAC:

1) Figuring out the balance between pricing and sales complexity. If you know that you have a complex product that cannot easily be sold without extensive sales person involvement, you can work out a rough minimum price range that you need to charge to get a decent payback on that sales process.

DS: Let’s use an example to bring this idea to life. Imagine that you expect that you’ll need to use an inside sales person to walk customers through the needs analysis, product evaluation, and closing process. You estimate that the inside sales person will cost you around $120k per annum in OTE (On Target Earnings), which is $10k per month. You estimate that they might be able to close two accounts per month. Doing a very simple CAC calculation that excludes marketing costs, and sales management expenses our inside sales person costs are $10k per month + approx. 30% in additional overhead costs = $13k. If we want to follow my recommendation of recovering CAC in less than 12 months, with 2 customer sales per month, we can see that we need to charge $6.5K in gross margin per customer. Then that should be increased by a similar guess at what marketing costs should be, and a fair allocation of sales management costs (e.g. one sales manager for every 6-10 sales people).

You may believe you can close more than 2 customers per month, so you can lower pricing. But on the other hand, you might have a more complex sale where you need to use Sales Engineers for demos, proof of concepts, etc. That increases CAC, and therefore means you need to charge more.

2) Once you recognize the importance of CAC, and how it may force you to price your product higher than you’d ideally like, it gives you the awareness of how damaging it is to your business to have a complex sales process. Armed with that realization, there are many things that you can do to simplify the sales process and lower CAC. For example, can you create a freemium version? Or if you are using a free trial, can you simplify that free trial by providing guided instructions to help the prospect get to the Wow! moment faster and with less work?

A note on accuracy/decimal places

The data that flows into calculating LTV:CAC is going to be lumpy and messy- in some ways it is almost insulting to compress all the minutiae of a successful sales process into a single ratio, helpful as it may be. To rephrase one of my favorite Peter Thiel quotes: LTV:CAC ratios are to be used, not believed. They help us take that data and make it actionable, but we should not fall into the mistake of treating them as gospel. A LTV:CAC ratio of 3.14159:1 is slightly better than 3:1. 3.1:1 is also slightly better than 3. I’ve never seen a situation where more than a single decimal place is useful for making a decision.

Finally, on communicating to investors

Lastly, a quick note on how to communicate to investors. When companies pitch to us at Matrix and LTV:CAC is part of the equation, we’re looking for a few key things. A strong LTV:CAC ratio is a plus of course, but very few companies come with pitch decks displaying subpar ratios. What we’re really looking for is evidence that the founder understands the logic behind the calculation, and has a smart way of thinking about how it might change as the company grows.

Ultimately a successful startup will need to increase its go-to-market spend many multiples of what it is when we meet with them, and so the real call we are making is not “this company has a strong LTV:CAC in the last year, A+” but rather “this company has broad product-market fit and its strong LTV:CAC today is likely sustainable at similar levels over time.” Founders on the top of their pitching game will use their data not as a chest-thumping vanity metric on a throwaway slide, but rather as a tool to demonstrate their robust understanding of the underlying unit economics of their business and how they tie into plans for future growth post-funding.

In conclusion

We hope this was helpful in correcting some of the common misconceptions out there and thinking through how to use this powerful metric effectively. We’re more than happy to answer follow-up questions in the comments, and welcome any criticism or counterpoints. Cheers!