For the seventh year in a row, we’re proud to work with KBCM Technology Group (formerly Pacific Crest Securities) to share results from a survey of ~385 private SaaS companies.

Thank you to the readers of forEntrepreneurs who participated in taking the survey! Thank you also to David Spitz (@dspitz) and the team at KBCM Technology Group for their work on the survey.

Part One will look at the following (The full report can be downloaded here):

- Survey Participant Composition

- Growth Rates

- Go-To-Market and Sales and Marketing

- CAC Rations and CAC Payback

Representative statistics on the survey participants

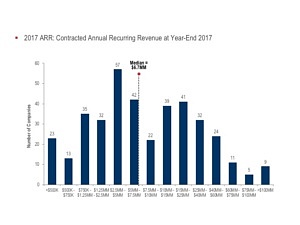

- $6.7MM median 2017 Ending ARR, with 81 companies >$25MM

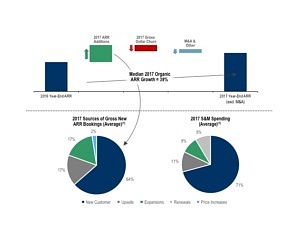

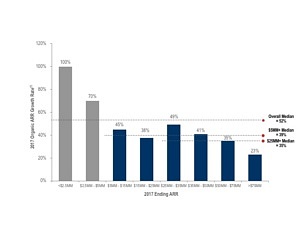

- Median organic growth in ARR in 2017 was +52% and +35% for companies >$25MM

- Median Employees (FTEs): ~70

- Median Customer count: ~325

- ~$20K median annual contract value

- 63% headquartered in the U.S

Some notable changes were made to this years survey. We asked respondents to provide precise numbers (vs. ranges) for certain key data such as ARR, churn and attribution of sales & marketing costs. Our Survey changes enabled us to calculate 2017 metrics directly.

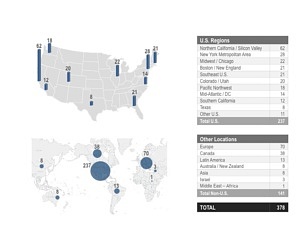

Survey Participant Composition

Survey Participate Geography

Survey Participate Distribution

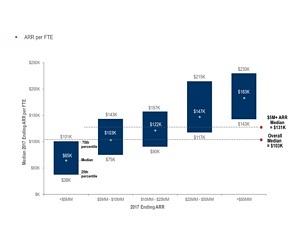

Human Capital Efficiency

Human Capital Efficiency

Respondents (ARR per FTE Efficiency): 384, <5MM: 160, $5MM-$10MM: 65, 10MM-25MM: 80, 24MM-50MM: 47, >50MM: 33

Growth Rates

Organic AAR Growth

(1) Excludes growth from M&A

Respondents: Total: 261, <$2.5MM: 53, $2.5MM-$5MM: 37, $5MM-$15MM: 64, $15MM-$25MM: 36, $25MM-$35MM: 20, $35MM-50MM: 22, $50MM-$75MM: 17, >$75MM: 12

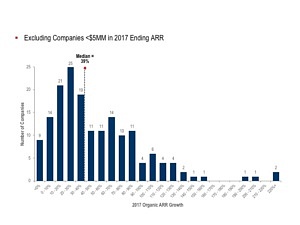

Organic Growth AAR Histogram

There’s a long and sparse “tail” for growth above the median, and hyper-growth is rare at scale.

How fast did you grow AAR organically in 2017

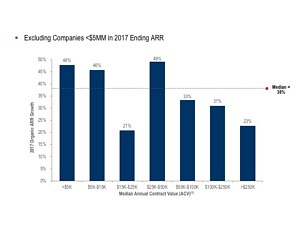

Median Growth rate as a function of contract size

Median Annual Contract Value (ACV): annual recurring SaaS revenues, excluding professional services, perpetual licenses and related maintenance for the median customer contract

Respondents/Median ARR: Total: 144, <$5K: 21/$19MM, $5K-$15K: 25/$24MM, $15K-$25K: 15/$26MM, $25K-$50K: 28/$16MM, $50K-$100K: 27/$19MM, $100K-$250K: 20/$33MM, >$250K: 8/$21MM

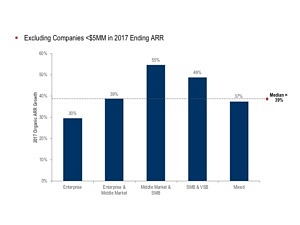

Median Growth Rate as a function of target Customer

(1)Target Customer Focus – At least 2/3rds of revenues come from designated customer base

Note: Enterprise customers defined as primarily targeting customers with >1000 employees, Middle market as 100-999 employees, SMB as 20-100 employees

and VSB as <20 employees

Respondents: Total: 171, Enterprise: 53, Enterprise & Middle Market: 61, Middle Market & SMB: 27, SMB & VSB: 14, Mixed: 1

- Companies focused on mid-market, SMB & VSB generally grow much faster than those focused strictly on enterprise customers.

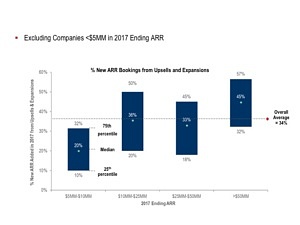

Reliance on Upsells and Expansions

Respondents: Total: 187, $5MM-$10MM: 47, $10MM-$25MM: 68, $25MM-$50MM: 41, >$50MM: 31

- Larger companies rely more heavily on upsells & expansions (“land & expand”) strategies – although it’s rare to see even the largest receiving more than 50% of bookings from such strategies

Go-To-Market and Sales and Marketing

Primary Mode of Distribution

(1)Primary Mode of Distribution defined by determining the greatest contributor to new sales and confirming that it is at least a 30% point higher contributor than any other. If no mode satisfies these conditions, then it is Mixed

101 and 184 respondents, respectively

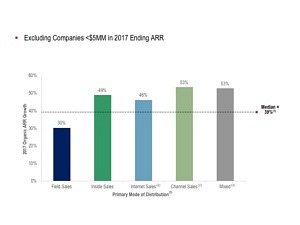

Median Growth Rate as a function of Sales Strategy

(1)Discrepancy from 40% median on slide 6 due to smaller set of respondents answering both questions

(2)Results may be skewed by small respondent sample size

Respondents/Median ARR: Total: 163, Field Sales: 78/$18MM, Inside Sales: 44/$19MM, Internet Sales: 7/$24MM, Channel Sales: 6/$18MM, Mixed: 28/$24MM

-

Companies relying predominantly on field sales tend to grow more slowly than those relying predominantly on inside sales. Mixed models also show higher growth. While internet and channel are also strong, the data is too sparse to be conclusive.

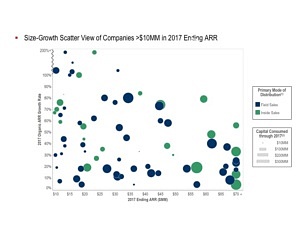

Distribution Strategy, Growth, and Capital Efficiency

(1) Capital consumed defined as total primary cumulative equity raised plus debt drawn minus cash on the balance sheet (adjusted for dividends / distributions)

80 respondents

- A look at the scatter chart comparing field vs. inside-led GTM strategies doesn’t reveal any clear patterns defining growth, capital consumption and size – each has their champions.

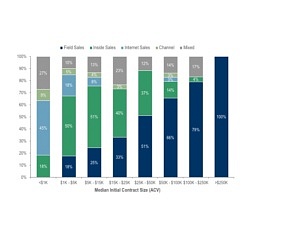

Primary Mode of Distribution as a function of median Initial contract size

Respondents: Total: 239, <$1K: 11, $1K-$5K: 40, $5K-$15K: 53, $15K-$25K: 30, $25K-$50K: 43, $50K-$100K: 29, $100K-$250K: 24, >$250K: 9

Respondents: Total: 239, <$1K: 11, $1K-$5K: 40, $5K-$15K: 53, $15K-$25K: 30, $25K-$50K: 43, $50K-$100K: 29, $100K-$250K: 24, >$250K: 9

- Analyzed by median initial contract value, field sales dominates for companies with median deals over $50K. Inside sales strategies are most popular among companies with $1K-$25K median deal sizes.

Analysis of field vs. inside sales in key crossover deal size tiers

(1)The % of dollar ARR under contract at the end of the prior year which was lost during the most recent year (excludes the benefits of upsells and expansions)

(2)The % change in ACV from existing customers, resulting only from the effect of churn, upsells / expansions and price increases

(3)Fully-loaded sales & marketing spend divided by new ARR components excluding churn

Respondents: Total: 63, Field-Dominated: 31, Inside-Dominated: 32

-

For companies with mid-sized contracts, those who choose inside sales over field: (1) grow faster (47% vs. 28%), despite being larger ($20M ARR vs. $10M); (2) have greater annual gross dollar churn (14% vs. 10%), but similar net dollar retention (100% vs. 102%); yet (3) have lower blended CAC ratios ($1.06 vs. $1.34).

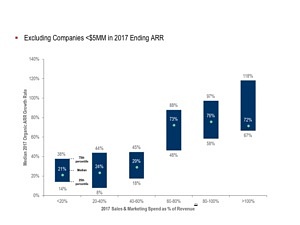

Sales and Marketing spends vs. growth rates

Respondents: Total: 159; <20%: 18, 20-40%: 49, 40-60%: 42, 60-80%: 26, 80-100%: 14, >100%: 10

-

Companies spending more on sales & marketing grow faster, but there appear to be diminishing returns above the 60-80% S&M / Revs. spending levels.

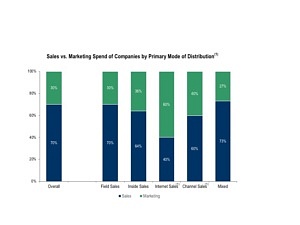

S&M Composition: Sales vs. Marketing Cost

Respondents: Overall: 165, Field Sales: 74, Inside Sales: 51, Internet Sales: 10, Channel Sales: 5, Mixed: 25

- The median company devotes 30% of S&M expenses to marketing. However, internet sales-driven companies rely more on marketing at 60%. Surprisingly, the median inside sales- driven company shows only slightly more reliance on marketing than their field sales-driven peers.

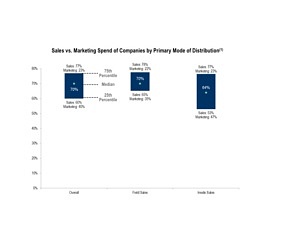

S&M Composition: Sales vs. Marketing cost close up

Respondents: Overall: 165, Field Sales: 74, Inside Sales: 51

-

A close-up view of the distribution of responses reveals that in fact many more inside sales-driven companies rely more heavily on marketing than their field sales-driven peers.

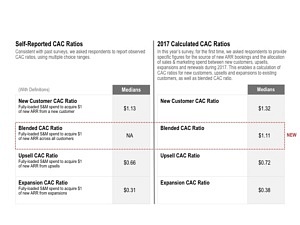

CAC Ratios and CAC Payback

Comparison of Self-reported vs. Calculated CAC ratios

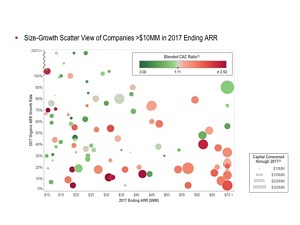

CAC and Capital Efficiency

(1)Capital consumed defined as total primary cumulative equity raised plus debt drawn minus cash on the balance sheet (adjusted for dividends / distributions)

105 respondents

-

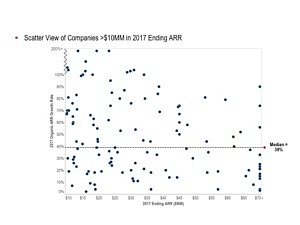

Notably, the fastest growing companies above the $10M ARR threshold tend to have lower CAC ratios. Interestingly, while low capital consumption ratios also appear to be correlated, there are a few notable exceptions (a few larger circles up and/or to the right).

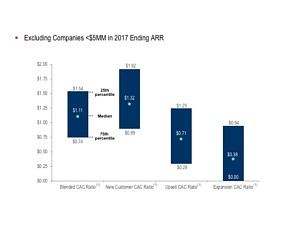

Distribution of 2017 Calculated CAC Ratios

Note: Based on calculated 2017 CAC Ratios

Respondents: Blended CAC: 169, New ARR from New Customer: 163, Upsells to Existing Customer: 127, Expansions: 115

- Median new customer CAC of $1.32 is almost double upsell CAC ($0.71) and over 3.0x expansion CAC ($0.38). The median blended CAC of $1.11 provides an all-in benchmark.

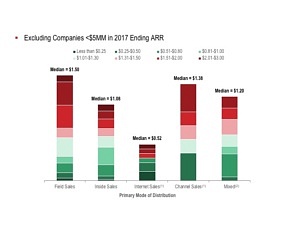

New Customer CAC Ratio by primary mode of distribution

Note: Based on calculated 2017 CAC Ratios

(1)Results may be skewed by small respondent sample size

Respondents: Total: 163, Field Sales: 78, Inside Sales: 48, Internet Sales: 8, Channel Sales: 7, Mixed: 22

- As expected, the new customer CAC ratio for field sales is significantly higher than all other sales strategies, in some cases by a large margin.

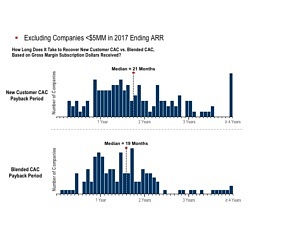

CAC Payback period (Gross Margin Basis)

(1)Implied CAC Payback Period: Defined as # of months of subscription gross profit required to recover the fully-loaded cost of acquiring a customer; calculated by dividing calculated CAC ratio by subscription gross margin

Respondents: New Customer CAC Payback: 138, Blended CAC Payback Period: 142

-

CAC payback provides a more intuitive measure of customer acquisition economics. On a gross margin basis, the median of just over 1.5 years for blended CAC payback provides a useful benchmark.