For the seventh year in a row, we’re proud to work with KBCM Technology Group (formerly Pacific Crest Securities) to share results from a survey of ~424 private SaaS companies.

Thank you to the readers of forEntrepreneurs who participated in taking the survey! Thank you also to David Spitz (@dspitz) and the team at KBCM Technology Group for their work on the survey.

Part One will look at the following (The full report can be downloaded here):

- Survey Participant Composition

- Growth Rates

- Go-To-Market and Sales and Marketing

- CAC Rations and CAC Payback

- Operations

Representative statistics on the survey participants:

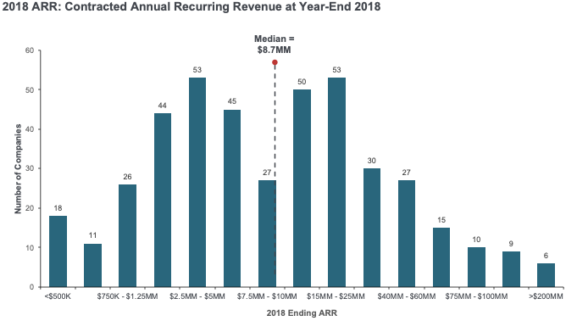

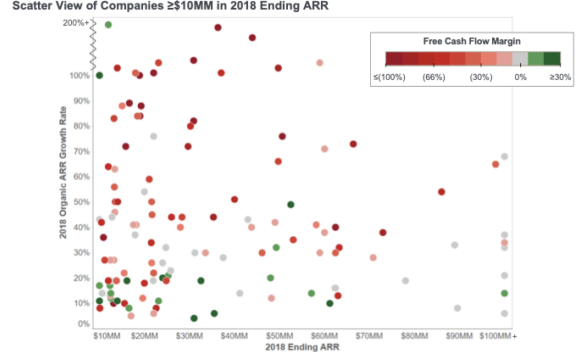

- $8.7MM median 2018 Ending ARR1, with 97 companies >$25MM

- Median organic growth in ARR in 2018 was +40% and +35% for companies >$25MM

- Median employees (FTEs): ~90

- Median customer count: ~300

- ~$28K median annual contract value

- 65% headquartered in the U.S.

Summary View of Median 2018 SaaS Metrics Performance

Respondents: Organic ARR Growth: 225, Sources of Gross New ARR Bookings: 214, Blended CAC: 197, 2018 In-Year Capital Consumption Ratio: 175, Cumulative Capital Consumption Ratio: 158, Gross Dollar Churn: 216

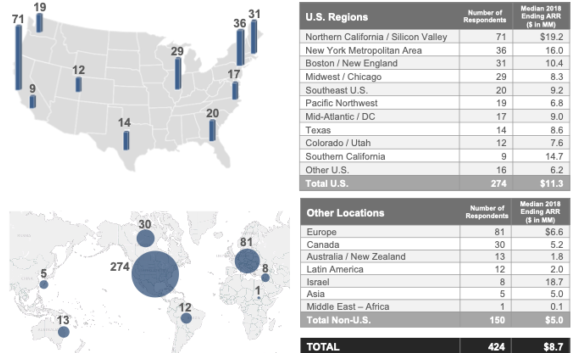

Survey Participant Composition

Survey Participant Geography (HQ)

Survey Participant Size Distribution

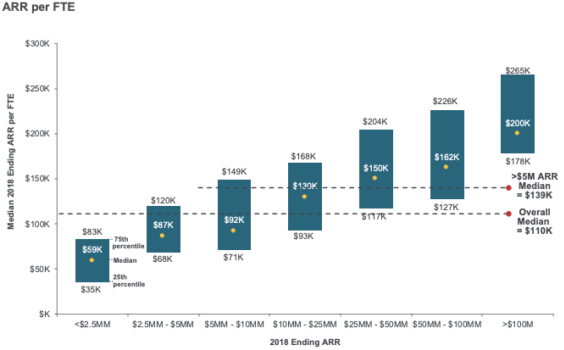

Human Capital Efficiency

Respondents (ARR per FTE Efficiency): 422, <$2.5MM: 99, $2.5MM-$5MM: 52, $5MM-$10MM: 71, $10MM-$25MM: 103, $25MM-$50MM: 46, $50MM-$100MM: 36, >$100MM: 15

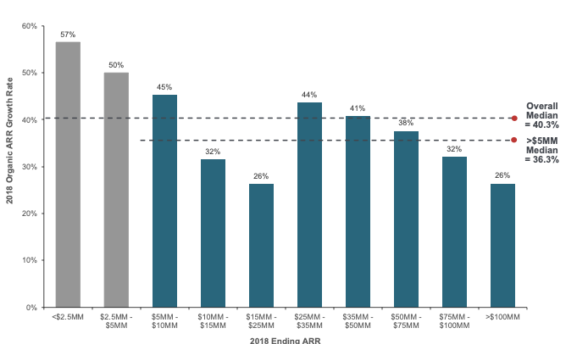

Growth Rates

Organic ARR Growth

Note: Excludes growth from M&A

Respondents: Total: 324, <$2.5MM: 60, $2.5MM-$5MM: 39, $5MM-$10MM: 57, $10MM-$15MM: 36, $15MM-$25MM: 47, $25MM-$35MM: 17, $35MM-50MM: 23, $50MM-$75MM: 25, $75MM-$100MM: 8, >$100MM: 12

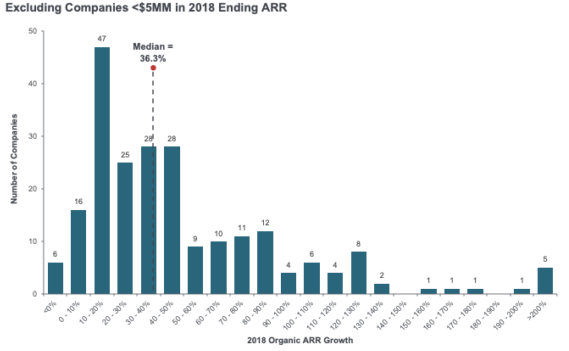

Organic ARR Growth Histogram

How Fast Did You Grow ARR Organically in 2018?

Note: Excludes companies with negative or no organic ARR growth

162 respondents

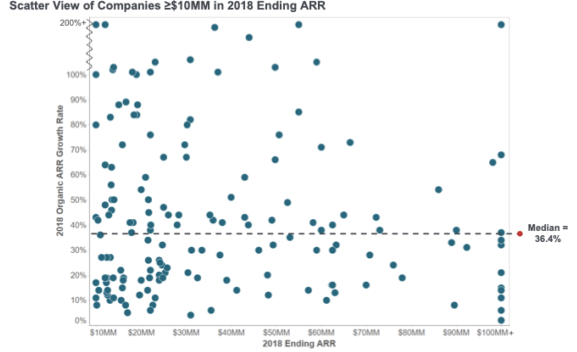

Growth vs. Burn Tradeoff

Note: Excludes companies with negative or no organic ARR growth

128 respondents

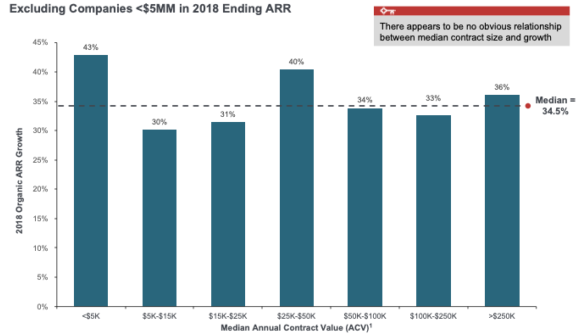

Median Growth As A Function Of Contract Size

Median Annual Contract Value (ACV): annual recurring SaaS revenues, excluding professional services, perpetual licenses and related maintenance for the median customer contract

Note: Median value may vary due to different sample population

Respondents/Median ARR: Total: 183, <$5K: 27/$14MM; $5K-$15K: 30/$13MM; $15K-$25K: 15/$18MM; $25K-$50K: 37/$16MM; $50K-$100K: 25/$19MM; $100K-$250K: 30/ $24MM; >$250K: 19/$33MM

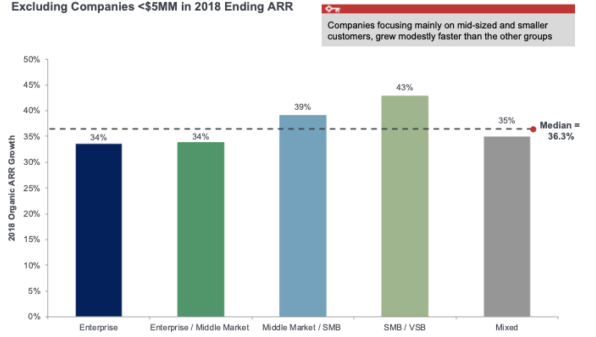

Median Growth Rate As A Function Of Target Customer

1 Target Customer Focus – At least 2/3rds of revenue come from designated customer base

Note: Enterprise companies defined as primarily targeting customers with >1000 employees, Middle Market as 100-999 employees, SMB as 20-100 employees and VSB as <20 employees

Respondents: Total: 225, Enterprise: 78, Enterprise / Middle Market & Middle Market: 85, Middle Market / SMB & SMB: 34, SMB / VSB & VSB: 17, Mixed: 11

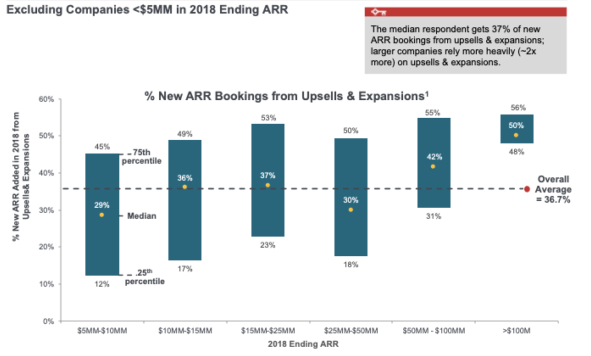

Reliance on Upsells & Expansions

1 Includes ~2.5% attributable to Price Increases

Respondents: Total: 214, $5MM-$10MM: 52, $10MM-$15MM: 35, $15MM-$25MM: 44. $25MM-$50MM: 39, $50MM-$100MM: 32, >$100MM: 12

Go-To-Market And Sales And Marketing

Primary Mode Of Distribution

1 Primary Mode of Distribution defined by determining the greatest contributor to new sales and confirming that it is at least a 20% point higher contributor than any other. If no mode satisfies these conditions, then it is Mixed

144 and 155 respondents, respectively

Median Growth Rate As A Function Of Sales Strategy

Respondents/Median ARR: Total: 141, Field Sales: 84/$22MM, Inside Sales: 40/$15MM, Mixed: 17/$24MM

Note: Internet Sales and Channel Sales excluded due to small sample size: Internet Sales: 3/$17MM, Channel Sales: 5/$12MM

Primary Mode Of Distribution As A Function Of Initial Median Contract Size

Respondents: Total: 251, <$1K: 7, $1K-$5K: 47, $5K-$15K: 42, $15K-$25K: 22, $25K-$50K: 48, $50K-$100K: 42, $100K-$250K: 28, >$250K: 15.

Analysis Of Field vs. Inside Sales In Key Crossover Deal Size Tiers

1 The % of dollar ARR under contract at the end of the prior year which was lost during the most recent year (excludes the benefits of upsells and expansions)

2 The % change in ACV from existing customers, resulting only from the effect of churn, upsells / expansions and price increases

3 Fully-loaded sales & marketing spend divided by new ARR components excluding churn

Respondents: Total: 44, Field-Dominated: 27, Inside-Dominated: 17

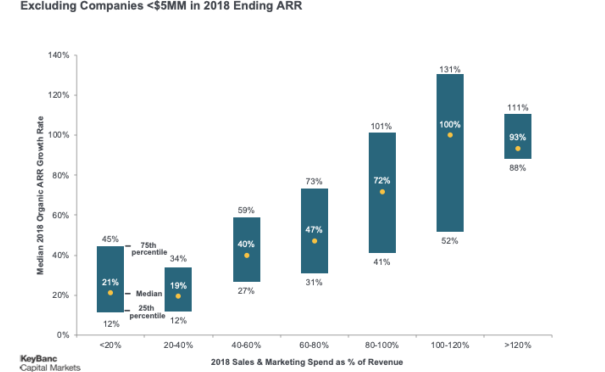

Sales & Marketing Spend vs. Growth Rate

![]()

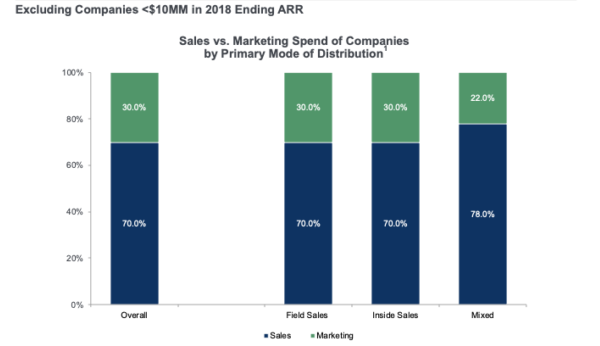

S&M Composition: Sales vs. Marketing Cost

Respondents: Overall: 132, Field Sales: 78, Inside Sales: 38, Mixed: 16

Note: Internet Sales 3 and Channel Sales 5, excluded due to small sample size

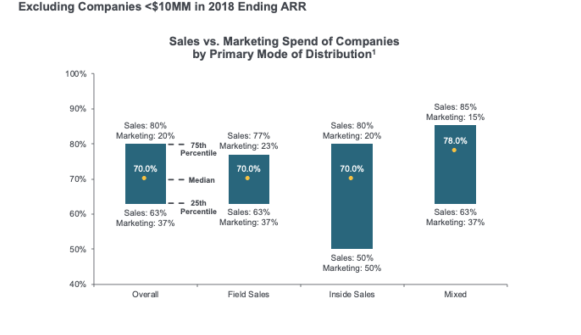

S&M Composition: Sales vs. Marketing Cost Close-UP

2 Respondents above the 75th percentile

3 Respondents below the 25th percentile

Respondents: Overall: 132, Field Sales: 78, Inside Sales: 38, Mixed: 16

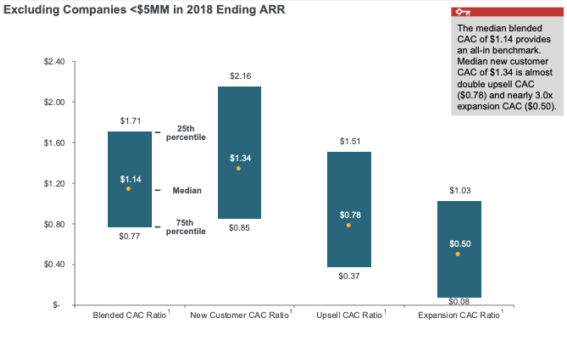

CAC Rations And CAC Paybacks

CAC Ratio Definitions

Note that we acknowledge some companies may believe it’s appropriate to assume a slight timing difference in their CAC Ratio analysis – S&M expenses determining future period ARR bookings, but for simplicity and consistency, we do not attempt to capture such assumptions here

Distribution Of 2018 CAC Ratios

Note: Based on 2018 CAC Ratios

1 See definitions on page 25

Respondents: Blended CAC: 197, New ARR from New Customer: 195, Upsells to Existing Customer: 152, Expansions: 137

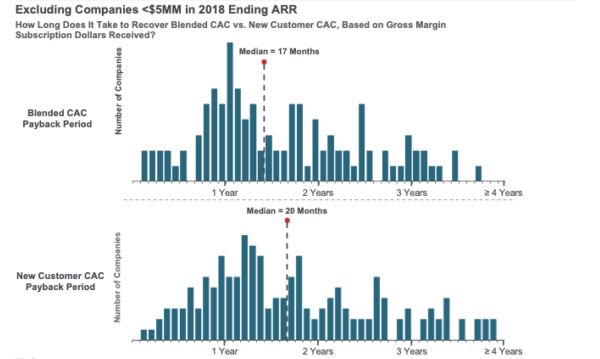

CAC Payback Period (Gross Margin Basis)

Implied CAC Payback Period: Defined as # of months of subscription gross profit required to recover the fully-loaded cost of acquiring a customer; calculated by dividing CAC ratio by subscription gross margin

Respondents: New Customer CAC Payback: 162, Blended CAC Payback Period: 175

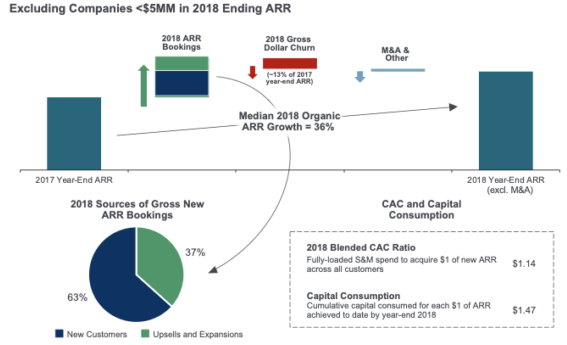

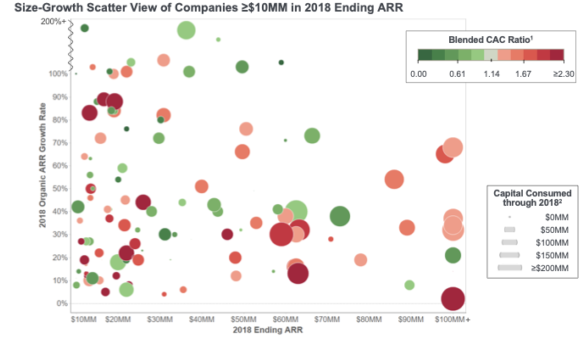

CAC And Capital Efficiency

2 Capital consumed defined as total primary cumulative equity raised plus debt drawn minus cash on the balance sheet (adjusted for dividends / distributions)

Note: Excludes companies with negative or no organic ARR growth

122 respondents

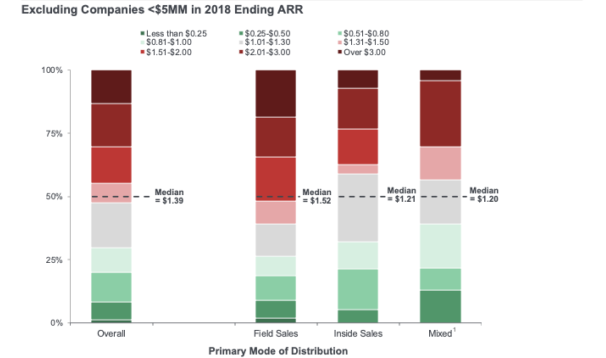

New Customer CAC Ratio By Primary Mode Of Distribution

Respondents: Total: 181, Field Sales: 102, Inside Sales: 57, Mixed: 22. Excludes Channel Sales: 6, Internet Sales: 8

Operations

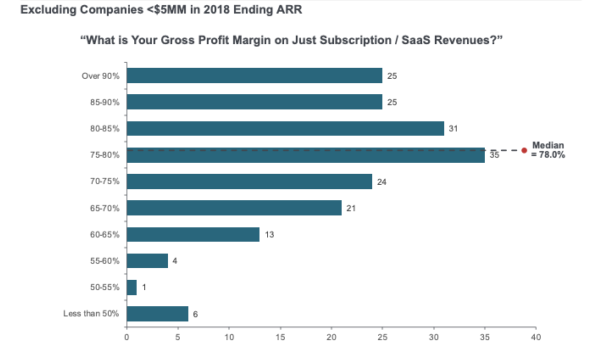

Subscription Gross Margin

185 respondents

Note: Respondents asked to back out stock-based comp. expenses and include customer support expenses

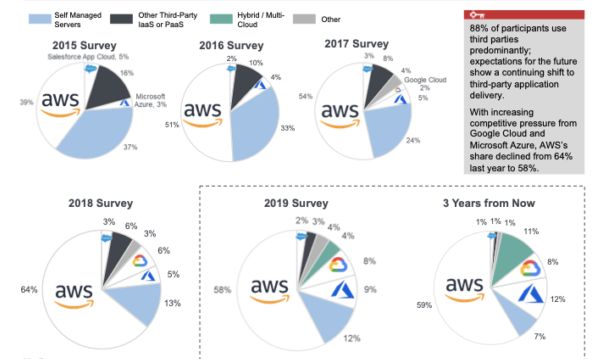

SaaS Application Delivery Trends Since 2014

Reported “predominant” mode of delivery

Respondents: 2014: 297; 2015: 282; 2016: 289; 2017: 384; 2018: 245; 2019: 274; 3 Years from Now: 270

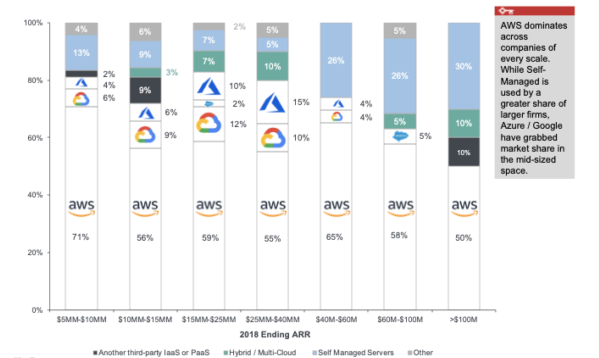

SaaS Application Delivery Mode As A Function Of Size Of Company

Respondents: Total: 192, $5M-$10M: 47, $10M-$15M: 32, $15M-$25M: 41, $25M-$40M: 20, $40M-$60M: 23, $60M-$100M: 19, >$100M: 10

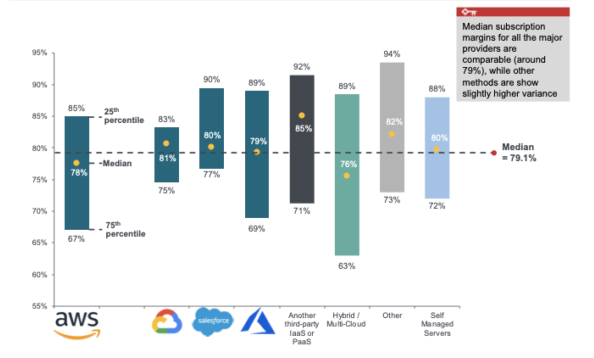

Subscription Gross Margin As A Function Of Application Delivery

Respondents: Total: 252, Amazon Web Services (AWS): 148, Google Cloud: 18, Salesforce: 5, Microsoft Azure: 23, Other Third-Party: 8, Hybrid / Multi-Cloud: 10, Others: 9, Self Managed Servers: 31

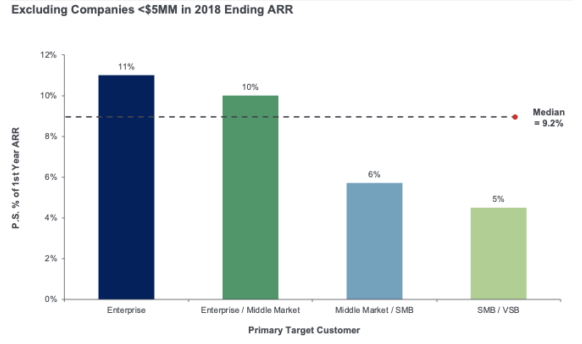

Professional Services (%Of 1st Year ARR) As A Function Of Target Customer

Respondents: Total: 137, Enterprise: 52, Enterprise / Middle Market: 56, Middle Market / SMB: 22, SMB / VSB: 7, excludes Mixed: 4, due to small sample size and respondents indicating no professional services

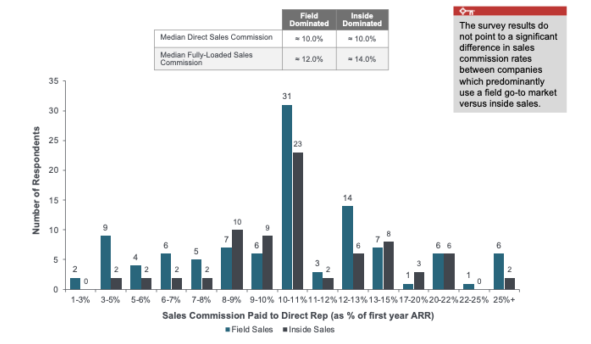

Analysis Of Sales Commission Levels

Note: For the definition of Primary Mode of Distribution, please see page 17

Note: Lower bound is inclusive

Respondents: Total: 208, Field Sales: 126, Inside Sales: 82

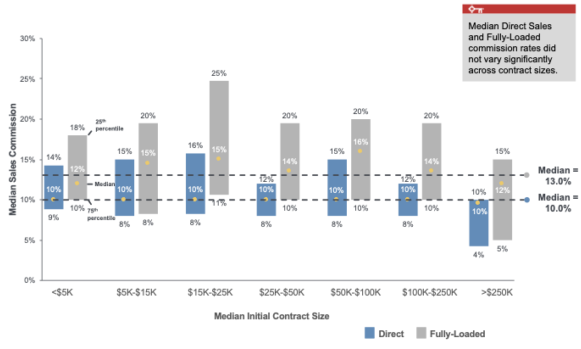

Sales Commissions As A Function Of Median Initial Contract Size

Respondents: Total: 222, <$5K: 38, $5K-$15K: 37, $15K-$25K: 20, $25K-$50K: 49, $50K-$100K: 31, $100K-$250K: 27, >$250K: 20

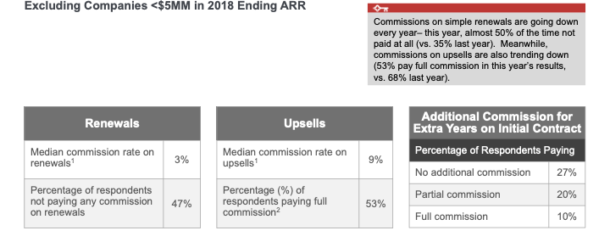

Direct Commissions For Renewals, Upsells and Multi-Year Deals